Nordics and India: Two Busy Ecosystems, One Quiet Corridor

How many founders in India actually talk about the Nordics – or founders in Denmark talk about India when they think about growing their startup? In my conversations over the last three years, the answer is: very few. Yet, if you look at the data, both startup ecosystems are vibrant: in the last three years there have been roughly 2546 Venture Capital (VC) deals in the Nordics and 3668 in India, with founders raising about $23B and $34B in venture funding respectively. But cross-border activity is tiny by comparison, only about 35 VC transactions between the Nordics and India, of which just 13 are from India to the Nordics. These are approximate numbers based on my own compilation from multiple data portals (Tracxn, Dealroom, KPMG and others), but they’re directionally clear: despite both ecosystems being very active globally, the Nordic-India VC corridor itself is still thin compared to the size of the opportunity.

How do Denmark–India Startup Collaborations Actually Happen?

If the Nordic–India VC corridor is still thin, the obvious question is: what can founders actually do today? Although the chart data includes all five Nordic countries, this post now narrows the lens to Denmark and the Indian startup corridor. A lot has already been written about student exchanges, academic collaborations and GCC (Global Capability Centre) models, so here I focus only on startups and venture-led collaboration.

The simple framework below is based on factual India–Denmark examples, written from an Indian founder’s point of view. The same patterns apply in reverse for Danish founders looking at India.

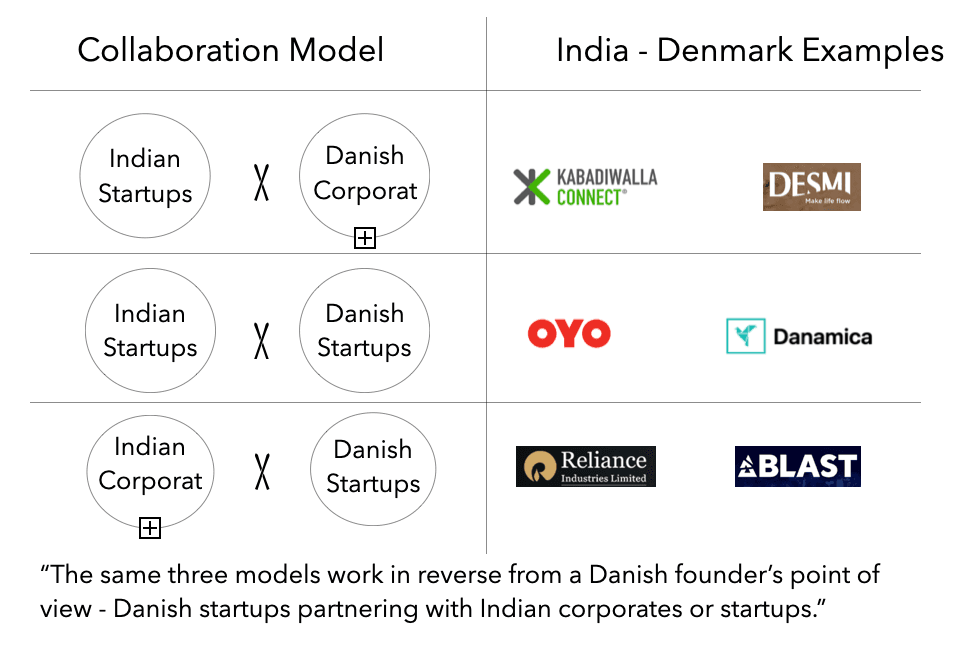

Indian startups × Danish corporates

Kabadiwalla Connect, an early-stage startup based in Chennai, and Desmi RoClean, a Danish corporation, have partnered to address plastic pollution by creating a circular economy for recycled plastic.

Indian startups × Danish startups

OYO, a Series G startup from India, acquired Danamica, a Danish early-stage SaaS platform for the residential rental market, and integrated its pricing engine into OYO’s global stack.

Indian corporates × Danish startups

RISE Worldwide, owned by Reliance Industries, has formed a joint venture with Denmark-based BLAST ApS in the esports segment.

Mash Makes is an Indo–Danish climate-tech startup, spun out of DTU in Copenhagen, that builds biofuel and biochar plants using Indian agricultural residue as its main feedstock. It reflects the reverse pattern: a Danish startup with Danish–Indian founders that chose to launch and scale in India, and is now backed by Danish corporate Norden.

These examples show that the corridor is already open in both directions. The next question, and the focus of the following sections: where are the most promising opportunity areas, starting with Life-science and Health?

Life-science and Health: India–Nordics Collaboration Still Early-Stage

How large is the Life-Science opportunity?

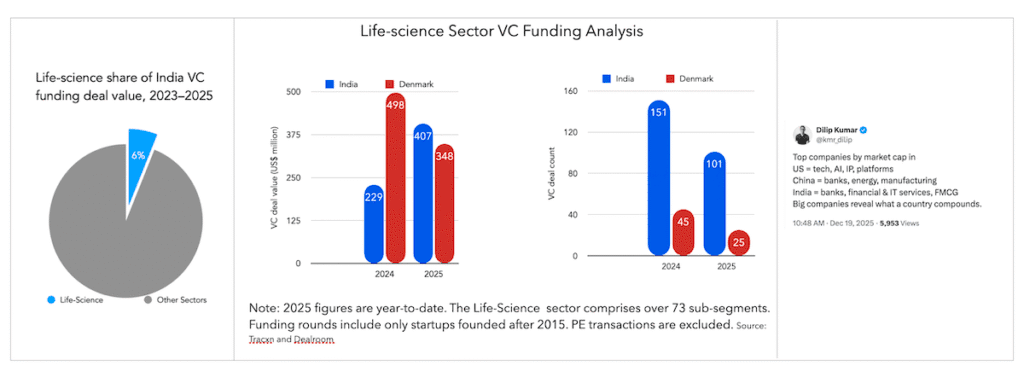

In this post, life-science includes HealthTech. Together, they span more than 70 sub-segments – from BioTech and MedTech to digital health – and all the charts use only VC deals in startups founded after 2015, excluding PE (Private Equity) and buyouts.

Looked at from the top, the Danish life-science sector already accounts for roughly one-third of the Danish venture capital market. In India, the picture is very different. Between 2023 and 2025, about 7,160 startups across all business sectors raised roughly US$31.1B in VC. Of these, 915 funding rounds and around US$2B went into life-science and HealthTech – about 6% of total VC funding.

Same Sector, Different Weight in the VC Mix

Historically, HealthTech has been one of the least funded categories in India (around 4–5% of VC in the decade from 2014 to 2024), but the last two years show a clear shift. As the Life-science Sector VC Funding Analysis chart shows, Indian life-science & HealthTech funding has grown from US$229m in 2024 to US$407m in 2025.

India is in the process of building a large HealthTech ecosystem. The ABHA ID (Ayushman Bharat Health Account) now covers more than half the country, with hundreds of millions of Indians able to link digital health records and use instant OPD registrations. Two of the biggest deals in HealthTech: Innovaccer (health-data intelligence and analytics, US$275m round) and PharmEasy (online pharmacy and healthcare platform, US$192 milion round) – demonstrate strong traction in this space. In other words, India has spent the last decade wiring up patient care, data and health-record rails. What has not seen comparable focus is life-science – drug discovery, core biotech and medtech R&D – where Denmark’s ecosystem, capital and companies are much more mature.

Indian VC preferences: curative vs preventive health

In my discussions with VCs in India, I still hear limited enthusiasm for life-science and HealthTech, especially on the preventive care side. Indian Venture Capitalists tend to favour curative categories – hospitals, diagnostics, and procedures that fit today’s fee-for-service model – over preventive or deep-science plays that take longer to commercialise.

Given this context, the natural question is: how can startups in both ecosystems collaborate? The same three collaboration models from the previous section apply directly here.

Three cross-border stories in Health & DeepTech

Danish MedTech × Indian hospitals

At the Nordic–India Startup Summit at TechBBQ, GO-Pen ApS, an early-stage Danish MedTech startup founded by Ole Nielsen, presented a user-fillable insulin pen that costs significantly less than what is currently available in India and is already approved by the FDA. This is a clear use-case where a large Indian hospital or hospital chain could partner with a Danish startup to localise, distribute and scale a clinically proven innovation.

Indian BioTech × Danish clinical ecosystem

Indian BioTech startup Zumutor Biologics, led by Founder and CEO Kavitha Iyer Rodrigues, is looking at Denmark for its clinical trials. After visiting Denmark, she shared on LinkedIn that Denmark is a strong launchpad for clinical validation and access to the wider Nordic biotech ecosystem.

Indian Quantum Computing × Early-stage drug discovery

QpiAI, which visited TechBBQ in August 2025, is an India-based startup backed by the country’s sovereign fund. The company builds quantum–classical models and AI tools to run large-scale simulations on India’s first 8-qubit superconducting quantum computer, developed for educational and research use. QpiAI is now looking to work with pharma R&D teams that want to use these models to shorten early-stage drug discovery cycles and test more candidates in silico before moving to clinical work.

These kinds of pairings highlight the asymmetry: Indian VCs and providers are more comfortable backing curative, revenue-linked health businesses, while Denmark has built depth in preventative drug discovery, BioTech, MedTech and quantum technologies. For founders working on BioTech, preventive health or quantum-computing–driven drug discovery from India, using the Danish startup and pharma-R&D ecosystem as a launchpad – and for Danish startups, partnering with large Indian hospital networks and health-data rails – is one practical way to turn that difference into a shared advantage.

Battery Recycling & BESS: Complementary Strengths Between India and the Nordics

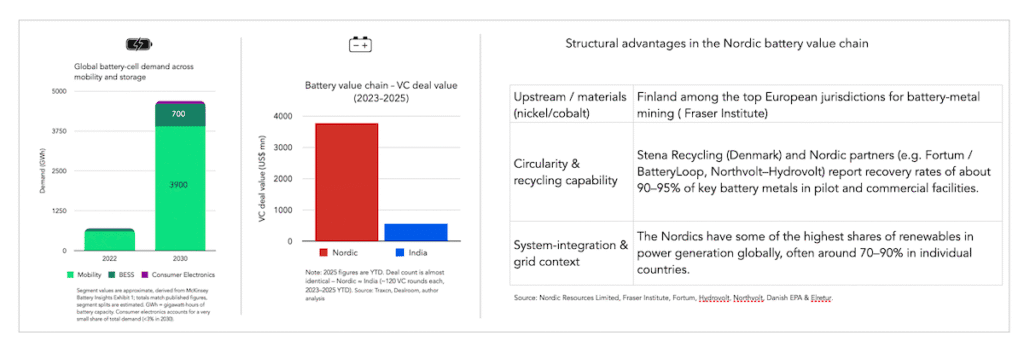

Between 2022 and 2030, global battery-cell demand is expected to rise from about 700 GWh to roughly 4,700 Gigawatt hours (GWh), with mobility accounting for ~3,900 GWh and stationary storage (BESS) for ~700 GWh. In the battery value chain, Nordic and Indian startups have closed a similar number of VC rounds (~120 each between 2023–2025), yet Nordic companies have raised around US$3.7B versus about US$550 million in India, with a higher share of later-stage firms in the Nordics.

Why should Indian battery-recycling founders look at the Nordics?

For Indian founders, this gap shows why collaboration matters: Nordic players bring upstream materials, recycling technologies that report 90–95% recovery of key metals, and experience operating in power systems with 70–90% renewables. In the long run, India’s EV and BESS build-out will create a significant end-of-life battery pool. That scale could become relevant for global recyclers – including Nordic players – looking for new markets, with Indian startups acting as local partners. Working together on the recycling value chain allows Nordic and Indian founders to combine scale on the Indian side with capital, technology and system-integration know-how on the Nordic side.

VC Dealflow Heatmap: Where the Corridor Still Has Whitespace

On the 2025 numbers, Nordic-India venture capital flow is still a rounding error: a small set of SaaS / fintech / gaming / consumer bets and just one MedTech deal, with no visible transactions yet in life-science or battery recycling / BESS. For VCs, that’s not a closed market; it’s an underwritten thesis waiting for sharper sourcing, stronger local partners and more deliberate cross-border syndicates.

This work has been shaped by the Nordic–India Startup Summit (NISS) at TechBBQ and the teams at the Embassy of India in Copenhagen, ICDK Bangalore, Novo Nordisk Foundation, and Kunal Singla at COBO Consult, whom I would like to thank for backing this corridor. I am also in active conversations with other key stakeholders across Denmark and India VCs, corporates, universities and ecosystem builders to deepen this Nordic–India startup bridge.

Disclosures, Caveats and Assumptions

- This is not a sponsored post and does not constitute investment advice.

- I have focused exclusively on startup and venture capital (VC) transactions, excluding private equity (PE) and buyouts.

- Funding numbers are approximate and compiled from multiple public databases (e.g. Tracxn, Dealroom, KPMG), so figures may differ slightly from other sources.

- I have referenced a few startups and funds from India and Denmark that I follow closely, so the examples are illustrative rather than exhaustive.

- Some startup names or data points might inadvertently be omitted.